Rowan Street 2025 Year-End Letter

- Alex Kopel

- Feb 4

- 11 min read

Dear Partners,

In 2025, Rowan Street generated a +11.1% net return, compared with +17.9% for the S&P 500. While we underperformed the index, we still delivered a solid absolute result following two unusually strong years. Over the past three years, Rowan Street has generated a cumulative net return of +252%, compared with a +78% total return for the S&P 500.

Rowan Street is a concentrated strategy built for long-term compounding, not for minimizing short-term volatility or closely tracking a benchmark. As a result, returns will differ meaningfully from year to year. Periods of underperformance are inevitable, just as periods of strong outperformance—such as in 2023 and 2024—are part of the same process. We believe individual years, viewed in isolation, are of limited significance; over time, results should reflect the compounding of intrinsic value at the business level.

Performance in 2025 was driven by our highest-conviction holdings. Tesla, a position we began building in the first half of 2025, was the largest contributor, adding approximately +6.8% to returns. Shopify and Spotify also contributed meaningfully, adding +5.6% and +4.5%, respectively. Meta Platforms, our largest holding, contributed +4.3% despite a disappointing fourth quarter (we discuss Meta in greater detail in a case study later in the letter).

Underperformance was largely attributable to The Trade Desk (TTD), which reduced returns by approximately -6.9%. While disappointing, TTD is now a much smaller weight in the portfolio. We continue to evaluate the business over a multi-year horizon rather than a single calendar year, and address our current thinking in a dedicated case study later in this letter.

The table below shows the annual returns of our largest holdings by portfolio weight as of December 31, 2025 and illustrates a simple reality of long-term investing: even exceptional businesses experience significant volatility.

Long Term Results

The table below summarizes Rowan Street’s annual results since inception, along with compounded returns over longer periods:

Over the past several years, Rowan Street has operated with a high degree of focus and discipline. We have remained invested in largely the same core group of businesses, allowing time and compounding to do the heavy lifting.

While stock prices moved sharply from year to year, the underlying companies continued to execute, strengthen their competitive positions, and grow intrinsic value.

The portfolio today reflects that discipline: a select number of high-quality businesses with strong balance sheets, durable economics, and the ability to reinvest free cash flow at attractive rates of return across cycles.

We make fewer decisions, own fewer companies, and hold them longer—so that long-term business performance, rather than short-term market movements, determines outcomes. This approach may not always look exciting in any single year, but we believe it is what allows results to compound favorably across full market cycles. The portfolio that follows reflects this philosophy in practice.

Our Portfolio: Long-Term Compounding in Action

The table below presents the Rowan Street portfolio as of December 31, 2025, ranked by portfolio weight. It reflects substantially all invested capital at that date and includes the date of initial investment and internal rate of return for each holding.

Case Studies in Capital Allocation and Temperament

Successful long-term investing does not require brilliance or a stratospheric IQ (fortunately for your fund managers). It requires a sound decision-making framework, a rational definition of risk, and—most importantly—the temperament to apply that framework consistently through both favorable and difficult environments. Many investment mistakes occur not because the framework is flawed, but because it becomes corroded under stress, crowd influence, or short-term performance pressure.

In the following case studies, we offer a practical view into how Rowan Street allocates capital and manages risk across different circumstances. Each example highlights a distinct aspect of our process: how we remain committed to a great business through severe pressure, how patience is often required long before results appear, how position size is allowed to adjust when leadership or fundamentals are tested, and how we act decisively when long-term opportunity finally presents itself. Together, they are intended to provide a clear picture of the framework and temperament that guide our decisions.

Meta Platforms (META): Letting Compounding Do the Work

Meta Platforms is our largest position. We first invested nearly eight years ago and have never sold a share. Over that period, the investment has compounded at approximately 19% annually.

Meta did not become a large position by design. It earned its weight over time as the business consistently grew revenues, earnings, and cash flow. As intrinsic value compounded, the stock price followed. As shown in the table below, the company’s fundamental growth broadly tracked the long-term return we achieved.

We did not trim the position simply because it became large. Many investors treat position size itself as a source of risk and respond by systematically reducing their most successful holdings. Our experience has been the opposite. Interrupting the compounding of exceptional businesses has been among the more costly mistakes we made earlier in our careers.

Charlie Munger captured this idea succinctly: “The first rule of compounding is to never interrupt it unnecessarily.” Peter Lynch expressed the same lesson more colorfully as “pulling out the flowers and watering the weeds.” Both observations reflect lessons learned through experience, not theory.

We think about risk differently than most investors. In our view, risk is not volatility, benchmark deviation, or position size. Risk is the probability of permanent capital loss. A durable, self-funding business with strong competitive advantages and owner-oriented leadership can be safer at a large weight than a weaker business held at a smaller one.

Mark Zuckerberg has a long history of prioritizing long-term competitive positioning over near-term earnings. Decisions that were initially unpopular — including the early shift to mobile and the acquisitions of Instagram and WhatsApp — ultimately proved foundational to the business we own today. We view the current investment cycle through the same lens: a deliberate effort to extend Meta’s competitive advantages over the coming decade rather than to optimize quarterly results.

Following Meta’s most recent earnings release, there was early evidence that these investments are already improving the effectiveness of the company’s core advertising platform, with benefits flowing through to engagement, monetization, and operating cash generation — even as free cash flow remains temporarily constrained by elevated capital expenditures. While we do not draw conclusions from a single quarter, the underlying economics are evolving in the direction we expected.

Meta has been a clear example of our core investment principle in practice: owning a select number of exceptional businesses and allowing compounding — rather than activity — to drive long-term results.

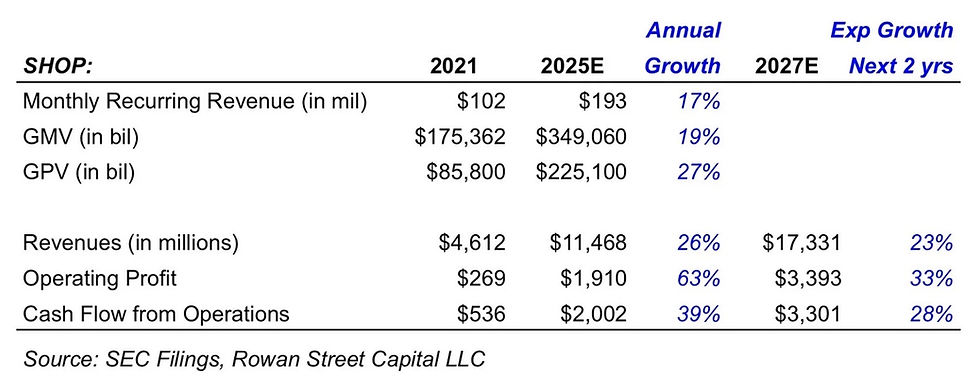

Shopify (SHOP): Patience Before Payoff

We initiated our investment in Shopify in the first quarter of 2022, after the stock had already declined more than 60% from its pandemic peak. Growth had slowed from extraordinary COVID-era levels, sentiment toward technology stocks had turned sharply negative, and valuation multiples were compressing across the sector. At the time, we believed we were paying a reasonable price for a high-quality business we had followed for many years.

After our initial purchase, the stock declined another ~50% as valuation multiples continued to contract. At its low point, Shopify traded near 7x sales—down from peak levels above 50x—despite the business continuing to grow revenues at a healthy rate and strengthen its competitive position. The drawdown reflected multiple compression rather than fundamental deterioration.

Throughout this period, Shopify continued to execute. Management refocused the business, improved efficiency, and prioritized long-term economics over short-term optics. Growth moderated to the mid-20% range, but the company’s merchant ecosystem expanded, merchant services deepened, and operating leverage gradually emerged.

Returns did not arrive quickly. For an extended period, the investment was down or flat while the business continued to compound. It was only in 2024—when Shopify generated over $1 billion in operating profit for the first time—that fundamentals became impossible to ignore.

As shown in the table below, our returns have been driven primarily by growth in revenues, operating profits, and cash flows rather than multiple expansion. Valuation multiples today are only modestly higher than when we first invested, despite significant volatility along the way.

Since our initial investment, Shopify has compounded at approximately 28% annually (as of December 31, 2025) and was our best performer in 2025, with the stock rising +51%. Shopify is a clear example of why patience—especially through periods of valuation compression—is often required before fundamentals are fully reflected in stock prices.

The Trade Desk (TTD): When Conviction Is Tested

We first invested in The Trade Desk in early 2020 because we believed it was building critical infrastructure for the open internet—an independent, asset-light, data-driven advertising platform with strong network effects, growing rapidly while remaining solidly profitable. The business executed well for many years, and as fundamentals compounded, the position grew organically from an initial weight of approximately 3% to over 12% of the portfolio at its peak.

During this period, conditions were favorable. Growth was consistent, industry tailwinds were strong, and execution appeared disciplined. Importantly, however, this was a phase in which the company—and its leadership—had not yet been tested by sustained adversity.

That test arrived in late 2024.

After peaking in December 2024, the stock declined sharply following its Q4 2024 earnings release, which included a rare revenue miss. Shares fell more than 30% in the immediate aftermath and continued to decline through 2025, as subsequent results and guidance failed to restore confidence. What followed was not a single reaction, but a broader reassessment—by us and by the market—of management’s communication, accountability, and adaptability under pressure.

Conviction is not declared. It is earned—often slowly, and usually through adversity.

Importantly, despite the severity of the drawdown, the investment remains profitable. From inception, the Trade Desk has compounded capital at a rate north of 10% annually, even after the decline. This is not a case of permanent capital impairment for us, but of moderated expectations and recalibrated conviction.

In our experience, many management teams perform well when conditions are accommodating. Far fewer demonstrate the clarity, transparency, and decisiveness required when growth slows, expectations reset, and credibility is questioned. It is during these periods that management character is revealed.

In The Trade Desk’s case, while leadership continued to emphasize long-term opportunity and total addressable market, investors sought clearer ownership of execution missteps, more concrete evidence of competitive share gains, and greater precision in communication. That gap mattered. Not because the long-term opportunity disappeared, but because trust and conviction are built—or eroded—during difficult periods, not easy ones.

As a result, while we continue to believe The Trade Desk remains a high-quality business with attractive long-term attributes, our conviction has moderated. We chose not to add to the position during the decline, nor to defend its prior portfolio weight. Instead, we allowed the position to adjust naturally as the market reassessed the business. Today, the position has returned to approximately its original percentage of the portfolio, though the capital invested remains meaningfully higher due to prior compounding.

This outcome was not the result of forced rebalancing or reactive decision-making. It reflects a core element of our process: the stocks that go up and become larger pieces of the portfolio have earned that right. The stocks that go down and become less significant have earned their fate. The portfolio wants to be in winners, and it will concentrate itself more and more into winners if you let it.

Certain businesses earn the right to become core holdings only after leadership has been tested through adversity. Meta earned that status within our portfolio over multiple cycles in which management demonstrated accountability, adaptability, and disciplined execution under extreme pressure.

Tesla (which we will talk about next) represents a different—but related—case. While it is still a relatively new position for us, the business itself and its leadership have already been tested through extraordinary adversity well before our investment. That history informed our willingness to initiate and size the position when the opportunity finally presented itself.

The Trade Desk remains under observation. Conviction will not be restored by market sentiment or valuation, but only if management demonstrates greater ownership of results, improved clarity in communication, and the ability to adjust strategy as conditions evolve.

Tesla, Inc. (TSLA)

Tesla is our newest core investment and was the only new position initiated during 2025. We began building the position during the first half of the year, at a time when sentiment toward the company was notably pessimistic and investor confidence was low.

We viewed this environment not as a signal of business impairment, but as an opportunity to establish long-term ownership in a company we believe possesses exceptional competitive advantages, deep first-principles engineering capabilities, and a culture oriented toward long-duration value creation. Tesla is led by a founder whose willingness to invest through uncertainty, endure prolonged adversity, and focus on difficult problems has, in our view, repeatedly reshaped entire industries.

Importantly, while Tesla has demonstrated resilience and execution across multiple cycles as a business, it has not yet proven itself within our portfolio, despite a short-term share price advance of more than 50% since purchase. As with all investments, its ultimate weight and role will be determined not by our intentions, but by the company’s ability to execute and compound intrinsic value over time.

We previously outlined our full investment thesis for Tesla in our Q3 2025 letter and encourage partners to review that discussion. From here, our role is one of patience and discipline — allowing long-term outcomes, rather than near-term sentiment or market volatility, to determine the result of this investment.

As with Meta and Shopify, we believe the most important contributor to long-term results will be our ability to avoid unnecessary interruption of compounding.

Looking Ahead

Today, our portfolio represents the strongest collection of businesses we have owned since inception. This is not because every holding has worked or markets have been cooperative, but because the portfolio has been allowed to evolve naturally over time. Businesses that have executed well through adversity have been permitted to grow in importance; others, where outcomes remain uncertain, have been allowed to recede without forcing action.

Over time, markets do a surprisingly good job of sorting businesses by quality if investors have the patience to let them. Our job is not to constantly rearrange the pieces, but to apply a consistent framework, define risk sensibly, and maintain the temperament required to let compounding work. The case studies in this letter reflect that approach in practice.

We remain focused on owning a select number of exceptional businesses, led by capable and tested management teams, and holding them long enough for their economics to reveal themselves. With that mindset, and with partners who share it, we believe the results will take care of themselves.

Thank you for your continued trust, partnership, and patience. It is a privilege to grow your capital alongside our own.

Warm regards,

Alex & Joe

DISCLOSURES

The information contained in this letter is provided for informational purposes only, is not complete, and does not contain certain material information about our fund, including important disclosures relating to the risks, fees, expenses, liquidity restrictions and other terms of investing, and is subject to change without notice. The information contained herein does not take into account the particular investment objective or financial or other circumstances of any individual investor. An investment in our fund is suitable only for qualified investors that fully understand the risks of such an investment. An investor should review thoroughly with his or her adviser the funds definitive private placement memorandum before making an investment determination. Rowan Street is not acting as an investment adviser or otherwise making any recommendation as to an investor’s decision to invest in our funds. This document does not constitute an offer of investment advisory services by Rowan Street, nor an offering of limited partnership interests our fund; any such offering will be made solely pursuant to the fund’s private placement memorandum. An investment in our fund will be subject to a variety of risks (which are described in the fund’s definitive private placement memorandum), and there can be no assurance that the fund’s investment objective will be met or that the fund will achieve results comparable to those described in this letter, or that the fund will make any profit or will be able to avoid incurring losses. As with any investment vehicle, past performance cannot ensure any level of future results. IF applicable, fund performance information gives effect to any investments made by the fund in certain public offerings, participation in which may be restricted with respect to certain investors. As a result, performance for the specified periods with respect to any such restricted investors may differ materially from the performance of the fund. All performance information for the fund is stated net of all fees and expenses, reinvestment of interest and dividends and include allocation for incentive interest and have not been audited (except for certain year end numbers). The methodology used to determine the Top 5 holdings is the largest portfolio positions by weight. The top 5 do not reflect all fund positions. The Top 5 can and will vary at any given point and there is no guarantee the fund will meet any specific level of performance. Net returns presented are net of fund expenses and pro-forma performance fees. Rowan Street Capital does not charge fixed management fees.

Comments