Rowan Street Q2 2025 Letter

- Alex Kopel

- Jul 12, 2025

- 7 min read

Updated: Jul 13, 2025

Dear Partners,

The first half of 2025 has been another strong period for Rowan Street. As of June 30, our fund is up +20.1% (net of fees) year-to-date, capping off a remarkable three-year run. Since mid-2022, we’ve compounded capital at approximately 51.7% (net) annually, delivering a +249% cumulative return. These are rare numbers, and while we don’t expect this pace to continue indefinitely, we believe it’s a powerful reflection of what’s possible when our investment philosophy is applied with discipline and patience.

This recent performance wasn’t the result of chasing fads or playing short-term games. It was earned by sticking to our process — one that has been sharpened over time through experience, mistakes, and reflection. Today, we run what we believe is our strongest and most focused portfolio to date, anchored by a small group of exceptional businesses and run by world-class entrepreneurs and owner-operators.

You can see our annual performance since inception and our compounded returns in the table below:

While our since-inception Internal Rate of Return (IRR) stands at approximately 9.4% (net), the long-term returns on each of our core holdings — all compounding at over 20% annually (see table below) — offer a more accurate reflection of the strength of our current investment process and the discipline we’ve built over the years. As we shared in our 10-Year Anniversary Letter, this evolution was shaped by experience and a few hard-earned lessons. But more than anything, it’s been our unwavering commitment to our guiding principles that has anchored us — and that discipline is now showing up in the results.

These principles are not just aspirational values — they’re the foundation of how we invest and the compass we follow every day. And they’re the reason our portfolio is now compounding the way we’ve always envisioned.

Our Portfolio: Long-Term Compounding in Action

Listed in the table below are our core holdings, sorted by the length of our holding period. As you can see, we have been shareholders of Meta Platforms (META) and Spotify (SPOT) for over 7 years — a holding period that we aim for when we make an initial purchase. Our internal rate of return (IRR) on both investments has exceeded 20% annually.

Netflix (NFLX) and The Trade Desk (TTD) have been in the portfolio for over 5 years and have delivered truly, in our opinion, spectacular returns. Topicus (CVE:TOI) and Shopify (SHOP), which we’ve owned for just over 3 years, have each compounded at over 22% annually — strong outcomes we believe are the result of thoughtful entry points and durable business quality.

Adyen (ADYEY) and Dino Polska (WSE:DNP) are our more recent investments, and both have worked out well so far. But as with all long-term investments, only time will tell whether they can live up to the high compounding bar set by our earlier holdings.

These are the types of businesses you don’t find often — and the opportunity to acquire them at a sensible price comes along only rarely. When you do, you let them run. That is the essence of our approach: to patiently compound capital by partnering with what we believe to be great businesses — and with some of the world’s best entrepreneurs and owner-operators — not by reacting to headlines or jumping from one narrative to the next.

Holding a Multi-bagger in a Portfolio

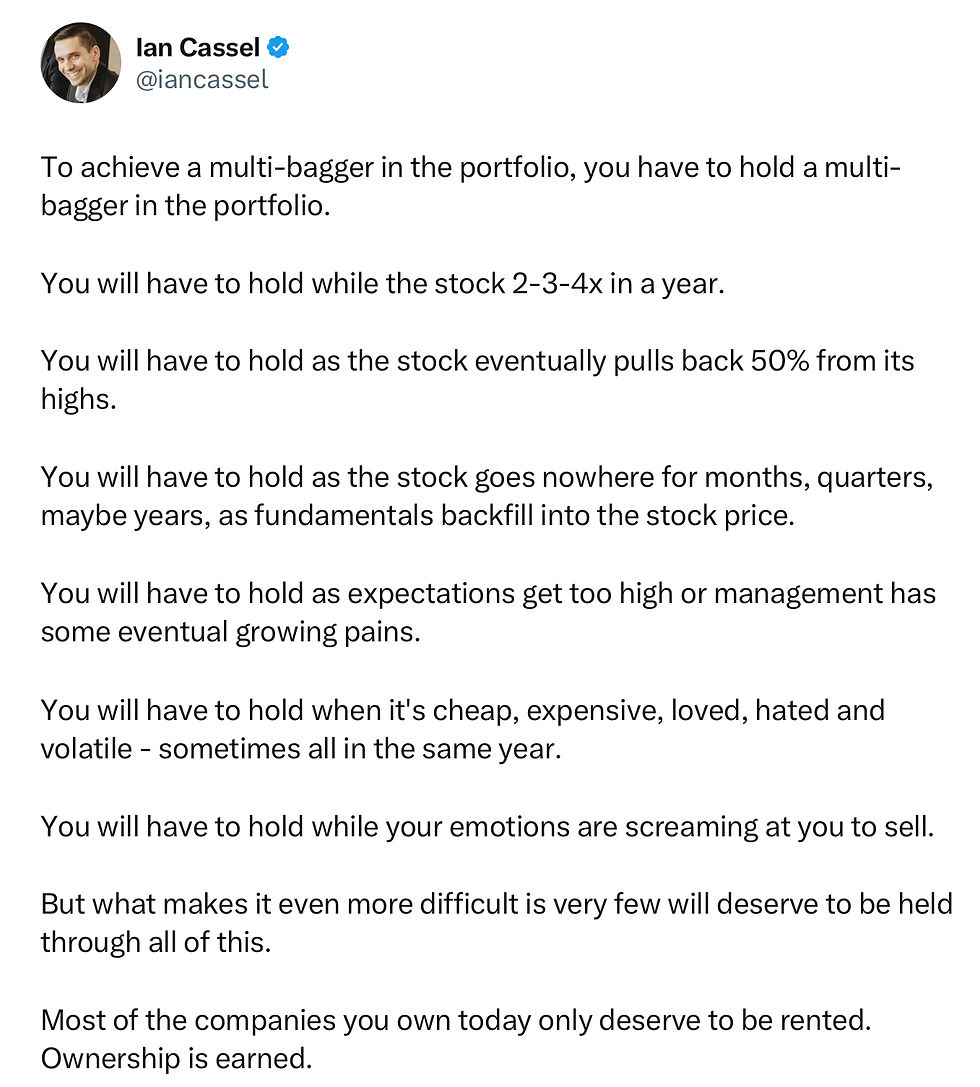

To kick off this section, we want to share a post from Ian Cassel (a respected professional investor and founder of MicroCapClub) that perfectly captures what it really takes to hold onto a multi-bagger:

This resonates deeply with our experience. Two of our longest-term holdings — Meta Platforms and Spotify — have each compounded at over 20% annually and generated over 4x returns for our fund over 7+ years. But the journey to those returns was anything but smooth.

Meta (META) saw a 40% drawdown early in our holding period, and then again dropped a staggering 75% in 2022 as sentiment around the business turned sharply negative. Conviction was tested. Headlines were brutal. Yet, we held on, grounded in fundamentals and our understanding of the business. At the time, we shared our perspective publicly in this article on Seeking Alpha: Does a $750 Billion Decline in Meta’s Market Cap Make Sense?, making the case for Meta when few wanted to touch it. That thesis was ultimately validated — Meta has since appreciated more than 7x from those lows, becoming one of the top contributors to our long-term performance.

Spotify (SPOT) might have been even more psychologically challenging. We first invested in 2018, and for a time the stock advanced meaningfully — only to then drop over 75% during the brutal 2022 drawdown. By 2023, five years into our holding period, our cumulative return on the position had round-tripped to zero. Imagine holding a company you deeply believe in for half a decade — and having nothing to show for it on paper. That’s a true test of conviction.

At the time, we published this article on Seeking Alpha: Spotify: A Favorite Idea That’s Extremely Mispriced, laying out our thesis while the stock was deeply out of favor — a thesis that ultimately proved to be both accurate and highly rewarding. From those 2022 lows, Spotify went on to appreciate nearly 10x, powerfully validating the discipline to stay the course.

Holding a multi-bagger isn’t about being right once — it’s about staying right long enough to make a meaningful impact on your long term track record.

Why We Exist — and Where Our Edge Lies

This is why we exist. Not just to identify the rare, extraordinary businesses worth owning — but to actually hold them through the emotional and psychological gauntlet that causes most investors to self-sabotage.

That kind of discipline — to sit still while the market tests your thesis, your patience, and your identity — we believe, is more valuable than any financial model, algorithm or forecast. And that, more than anything else, is our edge.

It’s the same edge we described in our 10-year letter this past March — and it bears repeating:

“We have no edge in predicting the economy, the Fed’s next move, or the stock market’s short-term direction. We’re not trying to call bottoms or tops, use leverage, trade options, or rotate between sectors. Our edge is in identifying greatness, buying it at fair prices, and then having the temperament to hold through the storms — while everyone else is losing their heads.”

We’re not here to be the smartest guys in the room. We’re here to avoid stupidity, stick to our process, and let time and compounding do the heavy lifting.

Our Edge in the Age of AI

In a world increasingly shaped by AI, it’s fair to ask whether this kind of edge — grounded in temperament, judgment, and long-term thinking — will still hold. We believe it will, perhaps more than ever. While AI can help investors process information faster, identify patterns in vast datasets, and even assist in building models, it doesn’t change human psychology. It won’t eliminate fear, greed, or the temptation to overreact.

AI might make the game faster and noisier, but it won’t change the rules of compounding. And in a world where everyone has access to the same data, models, and advanced tech, the differentiator is no longer who knows more — it’s who behaves better.

Looking Ahead

At Rowan Street, we’ve always believed that how you earn your returns matters just as much as the returns themselves. We’re not trying to build a hot streak. We’re building a long-term track record — one that’s earned through patience, discipline, and deep alignment with the businesses we own and the partners we serve.

As we look to the future, our ambition is to grow Rowan Street into a world-class investment partnership — not just in terms of size, but in the quality of the capital we manage and the relationships we build. Our long-term goal is to scale to $100+ million in assets, but we are committed to doing so the right way: one thoughtful, aligned partner at a time.

If you know investors who share our values — those who think in decades, not quarters; who care more about business fundamentals than headlines; and who want to be true partners in a long-term compounding journey — we would love to talk.

Thank you for your continued trust, partnership, and patience. It is a privilege to grow your capital alongside our own.

Warm regards,

Alex and Joe

Stay Connected with Us

We also publish our letters on Substack, where you can subscribe to receive future updates directly in your inbox. If our long-term approach resonates with you, we’d be honored to have you follow along and be part of the Rowan Street journey.

DISCLOSURES

The information contained in this letter is provided for informational purposes only, is not complete, and does not contain certain material information about our fund, including important disclosures relating to the risks, fees, expenses, liquidity restrictions and other terms of investing, and is subject to change without notice. The information contained herein does not take into account the particular investment objective or financial or other circumstances of any individual investor. An investment in our fund is suitable only for qualified investors that fully understand the risks of such an investment. An investor should review thoroughly with his or her adviser the funds definitive private placement memorandum before making an investment determination. Rowan Street is not acting as an investment adviser or otherwise making any recommendation as to an investor’s decision to invest in our funds. This document does not constitute an offer of investment advisory services by Rowan Street, nor an offering of limited partnership interests our fund; any such offering will be made solely pursuant to the fund’s private placement memorandum. An investment in our fund will be subject to a variety of risks (which are described in the fund’s definitive private placement memorandum), and there can be no assurance that the fund’s investment objective will be met or that the fund will achieve results comparable to those described in this letter, or that the fund will make any profit or will be able to avoid incurring losses. As with any investment vehicle, past performance cannot ensure any level of future results. IF applicable, fund performance information gives effect to any investments made by the fund in certain public offerings, participation in which may be restricted with respect to certain investors. As a result, performance for the specified periods with respect to any such restricted investors may differ materially from the performance of the fund. All performance information for the fund is stated net of all fees and expenses, reinvestment of interest and dividends and include allocation for incentive interest and have not been audited (except for certain year end numbers). The methodology used to determine the Top 5 holdings is the largest portfolio positions by weight. The top 5 do not reflect all fund positions. The Top 5 can and will vary at any given point and there is no guarantee the fund will meet any specific level of performance. Net returns presented are net of fund expenses and pro-forma performance fees. Rowan Street Capital does not charge fixed management fees.

Comments