Rowan Street Q2 2020 Letter

- Alex Kopel

- Jul 9, 2020

- 15 min read

Updated: May 28, 2021

Dear Partners,

Rowan Street Capital had a very successful second quarter of 2020. The fund returned +43.2% (gross) vs. S&P 500 increase of 20.5%. Year-to-date through June 30, the fund returned +20.5% vs. S&P 500 decline of (3.1)%.

Longer term, over the past 30 months, we have outperformed the S&P 500 by approximately 40% (please refer to the graph below). Since approximately 40% of our portfolio is invested in international companies, we have included the MSCI All Country World ex-U.S. Index that tracks large- and mid-cap non-U.S. equities. As you can see, we have outperformed global equities by 68% since the start of 2018.

Volatility and Market Timing

“Everyone has the brainpower to make money in stocks. Not everyone has the stomach.”— Peter Lynch

Below is a depiction of what happened in the stock market thus far in 2020. We can assure you that our performance this year was not derived from market timing or from some special ability to accurately forecast the movements in the stock market. The fund returned 20.5% while being fully invested throughout this crazy volatility.

We believe there is NO wealth creation without volatility! It is simply the “price of admission” that the market demands us to pay, yet there is so much effort on Wall Street that is dedicated towards minimizing volatility. These efforts are catered towards nurturing clients’ emotional well-being while creating an illusion of safety, but almost always come at a huge cost of reducing clients’ long term returns.

We are very fortunate to have limited partners in the fund that allow us to focus on the long-term compounding of their family’s capital instead of being distracted from our main goal in order to nurture their emotional well-being. This is a huge advantage for us!

Our Investment Process

“Give me six hours to chop down a tree and I will spend the first four sharpening an axe.”— Abraham Lincoln

We believe that a good investment process may not make you money in the short run, but will keep you in the game until the end. Contrary, a bad investment process may make you money in the short run, but will get you “killed” in-between. That is why we spent the first 3 years in the fund sharpening our axe: defining our investment approach and developing a simple, logical and repeatable process. We are very proud of the investment process that we have developed, and it's the hard work that we had put in our first 3 years of existence that set us up for success in the latter 2.5+ years, and we believe, for many years to come. The “Investment Performance” chart above shows our results since we have been fully invested into our strategy. From the beginning of 2018 though June 30th, the fund has compounded at 21% per annum in comparison to 8% per annum for the S&P 500.

Spotify (SPOT)

Spotify was the biggest contributor to our performance in 2020, and it has grown to be the biggest position in the fund (largely through capital gains). We first started buying shares back in May 2018 shortly after its IPO. We patiently waited for 2 years for Spotify stock to go up 90% in a matter of only two months, which compensated us handsomely for the wait.

Spotify opened for trading on the NYSE on April 3, 2018. Initial pre-trading reference price was US$132.00 per share and the opening price of the shares was US$165.90 per share, or approximately 25.7% higher than the NYSE reference price. As you can tell from the above graph, Spotify had lots of ups and downs over the past 2 years, but until the end of May 2020 the stock did absolutely nothing.

“Multi-baggers don't just go up. They also have sharp declines, they have long periods of stagnation as fundamentals backfill, old shareholders get bored, and new shareholders enter.” — @Ian Cassel

Psychologically, it's not easy to go through a two-year stagnation period in a stock (see graph above) while watching the market and its peers go up and up. What kept us in this position was our deep conviction in the company and its management. We have included a detailed write-up on Spotify and the evolution of the music industry in the Appendix at the end of this letter.

*****

Thank you again for your confidence and trust in our investment discipline. We appreciate the opportunity to grow your family capital alongside ours. We are currently open to new, thoughtful partners who appreciate our investment approach. If you know someone who you think would be a good fit for our strategy and Rowan Street Capital, please have them reach out to us.

As always, should you have any questions or comments, we would be very happy to hear from you. We look forward to reporting to you again at the end of 2020. Stay healthy and safe!

Best regards,

Alex and Joe

APPENDIX

Spotify Investment Thesis

Music Industry Background

When Spotify first launched its service in 2008, music industry revenues had been in decline, with total global recorded music industry revenues falling from $23.8 billion in 1999 to $16.9 billion in 2008. Growth in piracy and digital distribution were disrupting the industry. People were listening to plenty of music, but the market needed a better way for artists to monetize their music and consumers needed a legal and simpler way to listen.

As Spotify’s access model gained traction, however, that trend reversed itself in 2015 when global recorded music revenues grew more than 3% from the prior year. Growth accelerated in 2016, when global recorded music revenues reached $15.7 billion, an increase of 6% from 2015. This was the highest annual growth rate in 20 years, according to management estimates and industry reports.

In 2019, the global recorded music industry generated $20.2 billion in revenues, up 8.2% from the prior year $18.7 billion. Money generated by streaming accounted for more than half (56.1%) of all global recorded music revenues.

It’s very apparent from the graph above that streaming is the engine, which has primarily restored the global recorded music industry to growth. Streaming revenues increased by 4x since 2015, reaching $11.4 billion in 2019, while physical sales and digital download revenues continued to decline.

While streaming has changed the way many people access music, management believes there is an untapped global audience with significant growth potential. They believe the universality of music gives Spotify the opportunity to reach many of the 3.6+ billion internet users globally. There is opportunity for growth, even in more established markets. According to Nielsen, the average American listens to more than 32 hours of music each week, and there is significant room to capture additional share of these content hours. Research from MIDiA indicates that listeners who pay for streaming subscription services tend to consume more content hours on average than ad-supported users.

With the Ad-Supported Service, management believes there is a large opportunity to grow users and gain market share from traditional terrestrial radio. In the United States alone, traditional terrestrial radio is a $14 billion market, according to BIA/Kelsey. The total global radio advertising market is approximately $28 billion in revenue, according to Magna Global. With a more robust offering, more on-demand capabilities, and access to personalized playlists, Spotify offers a significantly better alternative to linear broadcasting.

Today, millions of people around the world have access to over 35 million+ tracks through Spotify, whenever and wherever they want. They are transforming the music industry by allowing users to move from a “transaction-based” experience of buying and owning music to an “access-based” model, which allows users to stream music on demand. In contrast, traditional radio relies on a linear distribution model in which stations and channels are programmed to deliver a limited song selection with little freedom of choice.

Overview

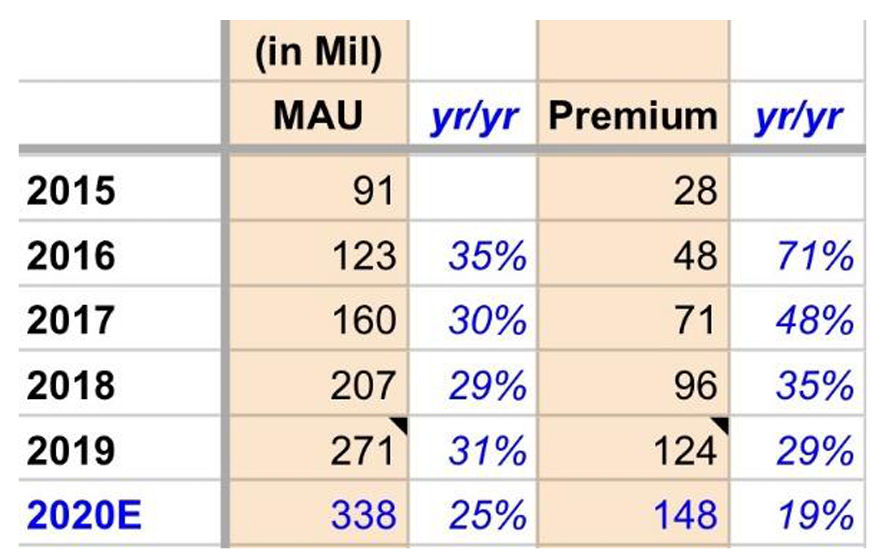

Today Spotify is the largest global music streaming subscription service. Their premium service provides Premium Subscribers with unlimited online and offline high-quality streaming access to their catalog. The Premium Service offers a commercial-free music experience. Their ad-supported service has no subscription fees and provides AdSupported users with limited on-demand online access to their catalog. As of March 31, 2020, Spotify platform had 286 million monthly active users and 136 million Premium subscribers as of December 31, 2017, which they believe is nearly double the scale of the closest competitor, Apple Music.

Spotify Users are highly engaged. The service gets monetized through both subscriptions and advertising. Both their Premium and the Ad-Supported users have been growing at 30%+ (see chart below). The Premium Service and Ad-Supported Service live independently, but thrive together. The Ad-Supported Service serves as a funnel, driving more than 60% of total gross added Premium Subscribers since they began tracking this data in February 2014.

Value Creation

Spotify founders set out to reimagine the music industry and to provide a better way for both artists and consumers to benefit from the digital transformation of the music industry. Spotify was founded on the belief that music is universal and that streaming is a more robust and seamless access model that benefits both artists and music fans.

Spotify is more than a music streaming service. Management believes they are in the discovery business. Every day, fans from around the world trust Spotify brand to guide them to music and entertainment that they would never have discovered on their own. Playlists have become the new discovery tool, and users are choosing to let them program more and more of their listening. If discovery drives delight, and delight drives engagement, and engagement drives discovery, Spotify wins and so do the users.

Sources of Moat

We believe that Spotify is in a position of strength because of their Freemium business model, their scale, superior user experience and content pipeline. The ubiquity of their platform is also a true advantage as Spotify is available in over 300 devices across 80 hardware brands. They are accessible to users even after listening habits have recently changed due to COVID lockdowns, where they have seen usage in car, wearables and web platforms fall, while their audience through TV and game consoles has grown materially. Personalization is another growing advantage. Many music services have large catalogs, but we believe Spotify is differentiated from other services because it provides users with a more personalized experience, driven by powerful music search and discovery engines. They have a large and growing base of users that are highly engaged on Spotify, which enables them to continuously learn about their listening behaviors throughout the day. They use this information to create a more personalized and engaging experience for each incremental visit to the platform. We believe this personalized experience is a key competitive advantage as users are more likely to engage with a platform that reflects their real-time moods and activities and captures a unique understanding of moments in their lives. As they further collect and process data and understand their users, technology will better understand and respond to users’ preferences, drive an even better overall user experience, and further differentiate Spotify service from its competitors.

Content Licensing

The vast majority of the content offered is licensed to Spotify on a non-exclusive basis. Management believes that personalization, not exclusivity, is key to their continued success.

From Barron’s article (April 2019): Before Spotify went public, labels signed deals that allowed the company to increase its gross margins from 13.4% to 25.5% from 2016 to 2018. Their equity stakes, and interest in seeing Spotify succeed to compete with Apple, gave the substantial incentives to do so. But there’s little evidence that central players will give the next inch quite so easily. Sony, which has initially taken the largest stake in Spotify, sold half of it last year, and Warner sold everything! Universal, the largest of the three, hasn’t announced any Spotify stock sales, but it is now going through its own transition. Vivendi plans to sell as much as half of Universal, and the company has been pitching itself to investors as a more valuable part of the music industry than Spotify (we completely disagree with this point!). Last year, Sony also bought EMI Music Publishing, which could further bolster its leverage. Spotify is girding for the next round of negotiations. “There was an economic self-interest of the record-label partners to allow the margin to increase, because, after-all, streaming has been the single source of renewed revenue growth to labels. So what was good for Spotify was good for the labels, and that's why the margin increased. Now, on a go-forward basis, is that what’s going to happen again? No, that's not going to happen again,” Spotify CFO Barry McCarthy (previously CFO at Netflix).

McCarthy outlined two paths to greater profitability:

Sell labels and artists new services like data about streaming habits. We personally believe that this is a huge edge that Spotify has over traditional labels where it has access to all this valuable data and listening habits that it can offer to artists, which can be very helpful to marketing, promotions and further content creation as well as better engagement with audiences. We think the historical value promotion of music labels could slowly fade away in the world of data and technology platforms.

Create new kinds of content - that’s where their podcast strategy comes in (we discuss this later).

Shifting Variable Cost to Fixed Cost

As of now, the biggest cost to Spotify’s business model is the Cost of Revenues, which is the royalties that it has to pay to three largest labels (paid out 3.9 billion Euros in 2018) compared to spending 493 million on R&D and 620 millions on sales & marketing. That prevents Spotify from leveraging its rapidly increasing revenues and having more profits go to the bottom line as with more streams they have to pay out more in royalties to music labels. Now, with podcasts it's a totally different business model. As they invest in their exclusive content and more people listen to it, it shifts the cost structure from variable to fixed and helps them create operating leverage.

In music, as Spotify CEO Daniel Ek emphasized, they don’t believe in exclusivity. In podcasts though, there is room for exclusivity and original content production and they will explore those opportunities. It fits really well within their dual-monetization strategy both ad-supported and subscription. On the Q4 2018 earnings call, Daniel Ek had to explain why it makes more sense to take ownership of spoken word content when they have historically been hesitant to own music content. He views them as two different businesses. Music industry is not a space where exclusivity makes sense. It’s difficult to keep things exclusive as artists and labels have an incentive to push the content out to as many places as possible because so much of an artists‘ s revenue comes from touring and concerts. However, audio and certainly podcasts are very different. Spotify is actively building out that market and it's at a very different stage of maturity, so they are heavily investing in where they think they can be one of the handful players in the space.

Podcasting Platform

Barry McCarthy on Q2 2019 Call: “Apple, of course, historically has been the largest player in the podcast space. They don't have an advertising business, and there has been no innovation in podcast advertising in its entire history. So ads get baked into RSS feeds and delivered to all listeners regardless of their interest in the demographic profile and any particular interest in any particular ad. So we're working hard on building digital ad sourcing technology, and we'll use that technology to dramatically revolutionize ad experience of podcast group listeners.”

Daniel Ek on new revenue opportunities: “We haven’t added internet-level monetization yet to audio. So, all the things you’ve come to expect in video and display in terms of measurability, in terms of just targeting, a lot of that is lacking in podcasts today. As you add these capabilities, you generally can revise price per ad impression because advertisers feel more certain about results they are getting. And if we do that, that's going to be a tremendous benefit for all podcasting creators, and it's also going to be a tremendous benefit for Spotify.”

Spotify has been aggressively building its podcast empire recently. In May, the company signed a multi-year licensing deal with Joe Rogan for exclusive rights to host full episodes of his popular podcast. More recently it reached a deal with Kim Kardashian West for a criminal justice podcast. Spotify has been focused on podcasts for more than a year, spending $600 million to snap up companies and content. So far it has also purchased Gimlet Media and the Ringer (podcasting-centric media with a string presence in sports). “I think we bought the next ESPN,” said Daniel Ek.

Spotify continues to see exponential growth in podcast hours streamed. Podcast adoption has reached almost 16% of total MAUs (monthly active users). The U.S. accounts for the largest share of podcast streams, but share of listening is higher and growing faster in several European countries. Podcast engagement is clearly a growing global phenomenon. For music listeners who do engage in podcasts, they are seeing increased engagement and increased conversion from Ad-Supported to Premium (exactly what they are trying to accomplish). Daniel Ek thinks they can bring a whole another game of monetization for podcasters, which will lead to overall growth of the podcasting industry.

In 2019, Spotify’s management outlined a vision to be the world’s largest audio platform. They now have more than 1 million podcasts on the platform compared to 0.25 million just a year ago (grew 3x). The best news for Spotify is that podcast users are more engaged overall and they do listen to more music as well (flywheel effect).

Valuations

Spotify had 91 million active users in 2015 and estimated to end 2020 with 338 million users (30% CAGR). There were 28 million Premium users in 2015 and at the end of 2020 they are estimated to be at ~150 million (40% CAGR). Just for comparison, Netflix ended 2019 with 167 million global subscribers. We believe Spotify can easily double their premium users to 300+ million by 2024, while growing their overall MAU (Monthly Active Users) to over 900 million.

Many investors have been concerned that Spotify’s premium ARPU (Annual Revenues Per User) has been in decline. In 2015 their ARPU was at 6.84 Euros and they finished 2019 with only 4.66 Euros in ARPU. At the end of 2020, that number is estimated to decline another 3% to 4.52 Euros. This is happening due to launches of their student and family plans at much lower price points. However, each of these plans have helped improve retention, according to management (premium churn has been steadily declining).

Daniel Ek: “From where I sit, when we look at the three dimensional chess board, factoring the better user experience we have provided, we don't see a decrease in revenue. In fact, the subscribers who are paying us at a lower ARPU are earning exactly the same lifetime revenue in Q4 2018 that they earned in Q4 2017 because churn has decreased. So, one divided by lower churn rate is more months of service at a lower ARPU is exactly to the dollar the same lifetime revenue, and now, it also happens that we have a higher gross margin on a year-over-year contribution basis, so profit from that same revenue stream is actually higher. The labels are earning the same amount of revenue they earned a year ago. Even though the price is down, we're growing faster and subscriber acquisition costs are down on a per subscriber basis.”

Spotify has grown its overall revenues from 1 billion Euros in 2014 to 6.8 billion in 2019 (44% CAGR). Revenues are estimated to grow to 7.9 billion Euros by the end of 2020. We estimate revenues can approach 19 billion Euros by 2024.

When we first started purchasing shares in 2018, the stock was trading at 3x Revenues. Even though, Spotify has been growing its revenues at astonishing rates, Mr. Market has been heavily discounting its multiples due to skepticism on the bargaining power that Spotify has over the fixed royalties that it has to pay out to the music labels. Gross Margins have been stuck at 25.5% for two years and the market was not optimistic about any margin expansion.

Recently, the price to revenue multiple has quickly gone up to 6x. In our view, what has happened is that Mr. Market has been pricing in the potential of a different revenue stream from Spotify Podcast Ads which, we believe, ought to produce relatively high gross margins for Spotify. It is built on existing technology and Spotify doesn’t have to pay royalty fees for content and is merely acting as a middleman for podcasters to fill their ad inventory. In addition, we think that exclusive podcast content strategy should drive increased overall user growth, which in effect should flex Spotify’s muscles over the music labels.

Management believes that over the long run it can expand its gross margins to 30%+. Netflix’ gross margins have been in the low 30s for a long time, until recently where GMs have grown to 38%. Netflix currently gets a 9x 2020 Revenue multiple, so current Spotify multiple of 6x is not unreasonable assuming management keeps executing.

A big part of Spotify’s valuations rely upon the future success of their podcasting strategy and their ability to sign up new users and to convert them into Premium Users. Even after the recent stock price increase, if management keeps executing, the stock should keep compounding at 15-20% CAGR over the next 5 years, in our view. So far, we believe Daniel Ek & Co. are going in the right direction!

DISCLOSURES

The information contained in this letter is provided for informational purposes only, is not complete, and does not contain certain material information about our Fund, including important disclosures relating to the risks, fees, expenses, liquidity restrictions and other terms of investing, and is subject to change without notice. The information contained herein does not take into account the particular investment objective or financial or other circumstances of any individual investor. An investment in our fund is suitable only for qualified investors that fully understand the risks of such an investment. An investor should review thoroughly with his or her adviser the funds definitive private placement memorandum before making an investment determination. Rowan Street is not acting as an investment adviser or otherwise making any recommendation as to an investor’s decision to invest in our funds. This document does not constitute an offer of investment advisory services by Rowan Street, nor an offering of limited partnership interests our fund; any such offering will be made solely pursuant to the fund’s private placement memorandum. An investment in our fund will be subject to a variety of risks (which are described in the fund’s definitive private placement memorandum), and there can be no assurance that the fund’s investment objective will be met or that the fund will achieve results comparable to those described in this letter, or that the fund will make any profit or will be able to avoid incurring losses. As with any investment vehicle, past performance cannot assure any level of future results. If applicable, fund performance information gives effect to any investments made by the fund in certain public offerings, participation in which may be restricted with respect to certain investors. As a result, performance for the specified periods with respect to any such restricted investors may differ materially from the performance of the fund. All performance information for the fund is stated net of all fees and expenses, reinvestment of interest and dividends and include allocation for incentive interest and have not been audited (except for certain year end numbers). S&P 500 performance information is included as relative market performance for the periods indicated and not as a standard of comparison, as it depicts a basket of securities and is an unmanaged, broadly based index which differs in numerous respects from the portfolio composition of the fund. It is not a performance benchmark, but is being used to illustrate the concept of “absolute” performance during periods of weakness in the equity markets. Index performance numbers reflected in this letter reflect reinvestment of dividends and interest (as applicable). Index information was compiled from sources that we believe to be reliable; however, we make no representations or guarantees with respect to the accuracy or completeness of such data.

Comments